Login

Login

The dangers and uncertainties of an unstable market are plentiful. Businesses struggle to find their footing and make all possible adjustments to survive the storm. We are seeing some recovery, but it’s no secret that the helicopter industry is still trying to cope with a depressed market. We’ve seen almost every possible situation play out during the downturn; from acquiring operational funds through the leveraging of assets, the sell-off of assets, returned leases, bankruptcy and restructuring, and some closing the doors completely. In almost all cases, an appraisal is required and depending on the situation, the parties involved are either looking for the highest possible values or the lowest possible values.

The pressures these businesses are experiencing are often passed along to the appraisal firm. Frequently, this is manifested in the appraisal request itself: requests for certain “types” of appraisals that would be misleading in a given set of circumstances, requests for a guarantee of a clients’ pre-determined opinion of value, changes in the definition of a type of value, approaching an appraisal assignment for a purpose for which it will not actually be used, etc.. An appraisal performed for the clients’ desired outcome rather than actual market conditions and for the proper purpose is not only misleading to any end user and takes away any real value in the appraisal, but it is also unethicaland comes with sometimes serious consequences.

Most notably, it is the inflated values that will cause the greatest damage down the road. Not only can inflated values skew an entire market segment, they can leave investors and lenders holding debt backed by assets that are worth much less than they think. We’ve repeatedly seen, over the history of the helicopter industry, the devastation this practice causes for everyone involved. While values which have been overly discounted may have somewhat less harmful effects, they still have a negative impact on true resale value for a particular model or a whole segment of the market, especially for models that are not frequently traded. They may also bring the wrath of the regulatory authorities with arguments of “bargain purchases” and the resulting tax implications.

Market perspectives will vary from one business to the next. An operator may have a different opinion than a private owner, who may have a different opinion than a lender or lessor. The appraiser exists to bring clarity to those varying perspectives by interpreting the value of the helicopter in relation to the market as it actually exists. Appraisers should come from a completely unbiased position, free from outside influences, using only facts, knowledge, and experience to develop an opinion of value. As a result, an appraiser will never be able to please every client’s value result expectations. Professional and ethical behavior is the only way the appraisal profession can maintain the public’s trust.

Appraisers and firms with inadequate qualifications or experience, or appraisers willing to purposely misrepresent values to satisfy the client’s specific needs tend to be more commonplace in a depressed market. It is important to make sure that you are not only employing a qualified and experienced appraiser, but one that maintains the highest standards. A reputable appraisal firm will not change their methodology and values to suit the needs of the client.

End users of an appraisal should take time to read the complete report. Note hypothetical conditions and assumptions, explanations of the methodology, definitions, and purpose used in the valuation process. Are all of these parameters appropriate for the situation and purpose? If the previous value results are available, compare them to the current value results. Significant value changes from one appraisal to the next may help identify potential issues. Watching for problem areas becomes even more important for lessors, lenders, and operators that require annual or bi-annual appraisals.

Differing appraisal methodologies, governing bodies, regulatory authorities, certifications and accreditations, U.S. Standards ( https://www.appraisalfoundation.org/ ) vs International Standards (https://www.ivsonline.org/), are all factors that influence how values are determined. Knowing your appraisal firm and its specialties is key to the accuracy of the values you will receive. While true market realities can be painful, knowing those realities, accepting them, preparing and dealing with them will not only ensure that the industry continues to have a healthy recovery, but it will help it recover faster, and avoid future negative effects of improperly and unethically performed appraisals.

About HeliValue$, Inc.

As pioneers of the helicopter appraisal process and methodology, HV$ has provided helicopter and parts appraisals for four decades. Our ASA accredited staff annually appraise over 2,500 helicopters. HV$ is the trusted advisor and industry-wide interpreter for an international clientele of manufacturers, vendors, helicopter operators, banks, leasing and insurance companies, and aviation law firms.

HV$ has also continually published The Official Helicopter Blue Book® since 1979. Information regarding specifications, current and historical resale values, current and historical manufacturer pricing, component overhaul and retirement intervals, and hourly maintenance costs are available for most of the 200 models covered in the Blue Book.

America continues to be the largest consumer of petroleum products with the European Union close behind. China is third but has the fastest growing demand. The United States consumes about 19,400,000 barrels of oil daily, the EU is at about 18,000,000, and China is at about 12,000,000.Everyone else is far behind, but next is India at about 4,200,000. India has the second largest population in the world with an estimated 358,000,000 under the age of 15. Mr. Clemente says this is the biggest reason that India’s economy and thus petroleum product use will continue to rise rapidly in the coming years.

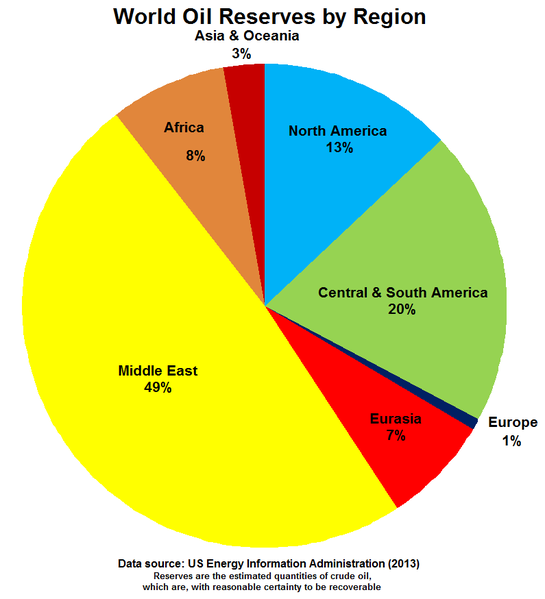

America continues to be the largest consumer of petroleum products with the European Union close behind. China is third but has the fastest growing demand. The United States consumes about 19,400,000 barrels of oil daily, the EU is at about 18,000,000, and China is at about 12,000,000.Everyone else is far behind, but next is India at about 4,200,000. India has the second largest population in the world with an estimated 358,000,000 under the age of 15. Mr. Clemente says this is the biggest reason that India’s economy and thus petroleum product use will continue to rise rapidly in the coming years. Overall demand for oil will, and has, gone up so why are prices staying at the $50-$52 per barrel range? One influence affecting where pricing sits today is the many sources of cheap-to-recover oil. In 1973, the eleven nation Organization of the Petroleum Exporting Countries (OPEC) shook the world by placing an oil embargo on the countries in the West who supported Israel. The members of OPEC, with the exception of Venezuela, were Islamic nations. Solidarity was never a question. OPEC had almost ⅔ of the then-estimated raw petroleum reserves of the World. Forty years later in 2013, estimated reserves had gone down to 49% as shown in the chart.

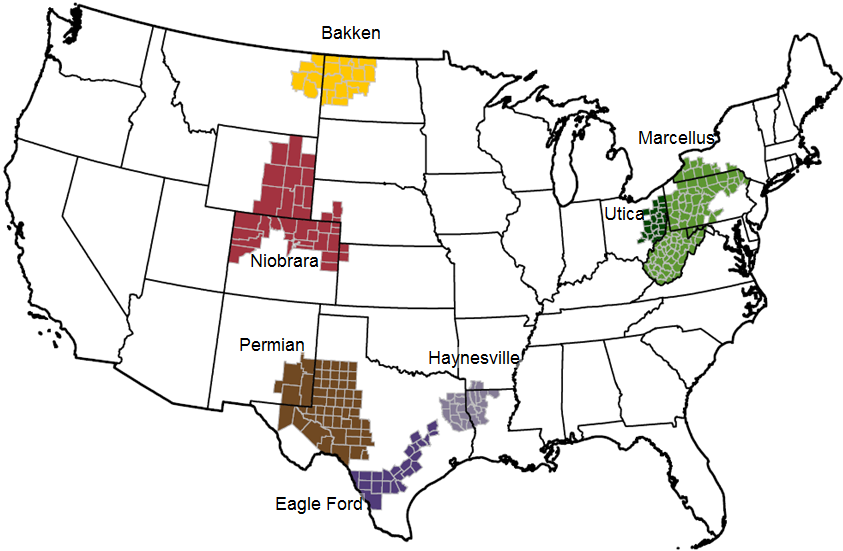

Overall demand for oil will, and has, gone up so why are prices staying at the $50-$52 per barrel range? One influence affecting where pricing sits today is the many sources of cheap-to-recover oil. In 1973, the eleven nation Organization of the Petroleum Exporting Countries (OPEC) shook the world by placing an oil embargo on the countries in the West who supported Israel. The members of OPEC, with the exception of Venezuela, were Islamic nations. Solidarity was never a question. OPEC had almost ⅔ of the then-estimated raw petroleum reserves of the World. Forty years later in 2013, estimated reserves had gone down to 49% as shown in the chart. The main reason that North America now has such large reserves is the viability of oil recovered by hydraulic fracturing. It was once thought that the price per barrel of oil had to be about $100 to make oil recovered by “fracking” economically viable. That was in 2011. The technology and techniques have improved every year. Oil prices had to be at $70 for fracking to be economical in 2014. In 2016 U.S. Energy Information Administration (EIA) commissioned HIS Global Inc. (HIS) to perform a study of upstream drilling and production costs. The report found that average well drilling and completion costs last year had fallen 25 to 30 percent below 2012 prices – the high point of the last decade.

The main reason that North America now has such large reserves is the viability of oil recovered by hydraulic fracturing. It was once thought that the price per barrel of oil had to be about $100 to make oil recovered by “fracking” economically viable. That was in 2011. The technology and techniques have improved every year. Oil prices had to be at $70 for fracking to be economical in 2014. In 2016 U.S. Energy Information Administration (EIA) commissioned HIS Global Inc. (HIS) to perform a study of upstream drilling and production costs. The report found that average well drilling and completion costs last year had fallen 25 to 30 percent below 2012 prices – the high point of the last decade. There were significant changes to helicopter values during our March 31, 2017, pricing meeting. The aircraft that had the most significant movement was the Sikorsky S-92 A. This is mostly due to the paucity of contracts in the North Sea. Obviously, the plunge in world oil prices in 2014 and the continuing low pricing per barrel of oil are the main reasons for the low helicopter activity. Another factor is the introduction of the “Super Medium” H175 and the AW189 in an already saturated market. The cost savings of leasing, buying, and operating the H175 or AW189 is giving them an edge compared over other heavies. There has also been an increased use of AW-139s where they can be employed over other aircraft. Regardless, any way you look at it, contract activity is very low and some available contracts are now requiring alternatives to the S-92A.

There were significant changes to helicopter values during our March 31, 2017, pricing meeting. The aircraft that had the most significant movement was the Sikorsky S-92 A. This is mostly due to the paucity of contracts in the North Sea. Obviously, the plunge in world oil prices in 2014 and the continuing low pricing per barrel of oil are the main reasons for the low helicopter activity. Another factor is the introduction of the “Super Medium” H175 and the AW189 in an already saturated market. The cost savings of leasing, buying, and operating the H175 or AW189 is giving them an edge compared over other heavies. There has also been an increased use of AW-139s where they can be employed over other aircraft. Regardless, any way you look at it, contract activity is very low and some available contracts are now requiring alternatives to the S-92A.

More information about the re-registration process, including a calendar for determining when your paperwork is due, is available on the

More information about the re-registration process, including a calendar for determining when your paperwork is due, is available on the